Frequently Asked Questions

A credit score is a number summarizing your credit risk, based on your credit data. A credit score helps lenders evaluate your credit profile and influences the credit that's available to you, including loan and credit card approvals, interest rates, credit limits and more.

FICO® Scores are the most widely used credit scores. Each FICO® Score is a three-digit number calculated from the data on your credit reports at the three major credit bureaus —Experian, TransUnion and Equifax. Your FICO® Scores predict how likely you are to pay back a credit obligation as agreed. Lenders use FICO® Scores to help them quickly, consistently and objectively evaluate potential borrowers' credit risk.

Not all credit scores are FICO® Scores. Because FICO® Scores are the credit scores most widely used by lenders—90% of top lenders use FICO® Scores—knowing your FICO® Scores is the best way to understand how potential lenders could evaluate your credit risk when you apply for a loan or credit. Other credit scores, which use scoring formulas different from FICO's, may not give you an accurate representation of the scores your lender uses when assessing your credit profile.

1. Mercator Advisory Group Analyst Report, 2018To keep up with consumer trends and the evolving needs of lenders, FICO periodically updates its scoring model, resulting in new FICO® Score versions being released to market every few years. Additionally, different lenders use different versions of FICO® Scores when evaluating your credit. Auto lenders, for instance, often use FICO® Auto Scores, an industry-specific FICO® Score version that's been tailored to their needs.

Between all three bureaus, there are 19 FICO® Scores that are most commonly used by lenders. Use the chart below as a guideline for which score version is most relevant for the type of credit or loan you're seeking.

| Experian | Equifax | TransUnion | |

|---|---|---|---|

| Widely used versions | |||

| FICO® Score 9 | FICO® Score 9 | FICO® Score 9 | |

| FICO® Score 8 | FICO® Score 8 | FICO® Score 8 | |

| Versions used in auto lending | |||

| FICO® Auto Score 9 | FICO® Auto Score 9 | FICO® Auto Score 9 | |

| FICO® Auto Score 8 | FICO® Auto Score 8 | FICO® Auto Score 8 | |

| FICO® Auto Score 2 | FICO® Auto Score 5 | FICO® Auto Score 4 | |

| Versions used in credit card decisioning | |||

| FICO® Bankcard Score 9 | FICO® Bankcard Score 9 | FICO® Bankcard Score 9 | |

| FICO® Bankcard Score 8 | FICO® Bankcard Score 8 | FICO® Bankcard Score 8 | |

| FICO® Score 3 | FICO® Bankcard Score 5 | FICO® Bankcard Score 4 | |

| FICO® Bankcard Score 2 | |||

| Versions used in mortgage lending | |||

| FICO® Score 2 | FICO® Score 5 | FICO® Score 4 | |

| Newly released version | |||

| FICO® Score 10 | FICO® Score 10 | FICO® Score 10 | |

| FICO® Auto Score 10 | FICO® Auto Score 10 | FICO® Auto Score 10 | |

| FICO® Bankcard Score 10 | FICO® Bankcard Score 10 | FICO® Bankcard Score 10 | |

| FICO® Score 10T | FICO® Score 10T | FICO® Score 10T | |

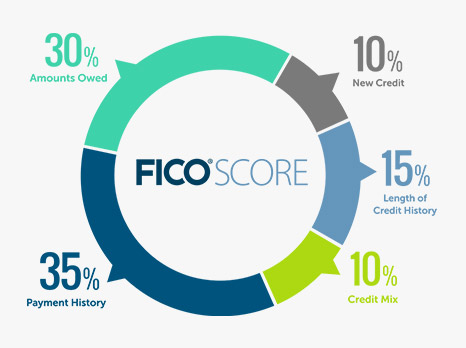

Your FICO® Scores are calculated from the credit data on your credit reports. Specifically, FICO® Scores consider 5 main categories of credit data from your reports: Payment history, amounts owed, length of credit history, new credit and types of credit in use. The chart below shows the relative importance of each category.

FICO® Scores generally range from 300 to 850, where higher scores demonstrate lower credit risk and lower scores demonstrate higher credit risk (note that industry-specific FICO® Scores have a slightly broader 250 — 900 range). What's considered a "good" FICO® Score varies by lender. For example, one lender may offer its lowest interest rates to people with FICO® Scores above 730, another lender only to people with FICO® Scores above 760.

The chart below provides a breakdown of ranges for FICO® Scores found across the U.S. consumer population. Again, each lender has its own credit risk standards, but this chart can serve as a general guide of what a particular FICO® Score represents.

| FICO® Score | Rating | What FICO® Scores in this range mean |

|---|---|---|

| < 580 | Poor |

|

| 580 — 669 | Fair |

|

| 670 — 739 | Good |

|

| 740 — 799 | Very good |

|

| 800 + | Exceptional |

|

No. While your FICO® Scores consider a wide range of information on your credit reports, they don't consider your income, age, education, employment history, gender, zip code, marital status or race. Any information not found on your credit reports, or any information not proven to be predictive of future credit performance, is also not considered by your FICO® Scores.

FICO's research shows that people with higher FICO® Scores tend to:

- Make all their payments on time, every month

- Keep credit card balances low

- Apply for new credit only as needed

- Establish a long credit history

FICO® Score Open Access is an educational program, launched by FICO and in partnership with lenders, with the goal of further educating individuals about their credit by increasing consumer access to FICO® Scores. Lenders participating in FICO® Score Open Access provide their customers free access to the FICO® Scores they use to manage credit accounts. If your bank, credit card issuer, auto lender or mortgage servicer is participating in FICO® Score Open Access , you can see your FICO® Scores—along with the top factors affecting your scores—for free.

You can make sure you're getting access to your FICO® Scores — and not a generic credit score — by obtaining your FICO® Scores directly from an authorized FICO® Score retailer or FICO® Score Open Access partner .